All Categories

Featured

Table of Contents

There is no payment if the policy expires prior to your death or you live past the plan term. You may have the ability to restore a term plan at expiration, yet the premiums will certainly be recalculated based on your age at the time of revival. Term life insurance policy is typically the least pricey life insurance policy available since it uses a death advantage for a limited time and doesn't have a cash money worth part like irreversible insurance coverage.

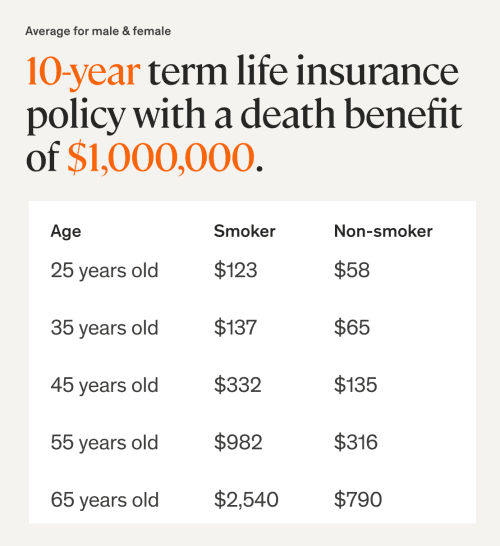

At age 50, the premium would certainly increase to $67 a month. Term Life Insurance Rates 30 years old $18 $15 40 years old $28 $23 50 years old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life plan, for guys and females in outstanding wellness.

Increasing Premium Term Life Insurance

The lowered danger is one factor that allows insurers to charge lower premiums. Rate of interest, the financials of the insurance policy company, and state regulations can also impact costs. In basic, firms commonly use much better rates at the "breakpoint" protection degrees of $100,000, $250,000, $500,000, and $1,000,000. When you think about the amount of protection you can get for your costs bucks, term life insurance policy tends to be the least expensive life insurance policy.

Thirty-year-old George wants to protect his family in the not likely occasion of his passing. He buys a 10-year, $500,000 term life insurance coverage plan with a costs of $50 monthly. If George dies within the 10-year term, the policy will pay George's beneficiary $500,000. If he dies after the plan has run out, his beneficiary will certainly receive no advantage.

If George is detected with an incurable health problem during the first plan term, he probably will not be qualified to renew the plan when it expires. Some policies offer ensured re-insurability (without proof of insurability), but such features come at a higher price. There are several sorts of term life insurance policy.

A lot of term life insurance has a degree costs, and it's the type we've been referring to in many of this write-up.

10 Year Renewable Term Life Insurance

Term life insurance policy is appealing to youngsters with youngsters. Parents can obtain significant coverage for an affordable, and if the insured passes away while the plan holds, the family can rely upon the fatality benefit to replace lost revenue. These policies are also fit for individuals with expanding households.

The appropriate option for you will rely on your needs. Right here are some things to think about. Term life plans are ideal for individuals that desire considerable insurance coverage at an inexpensive. Individuals that have entire life insurance policy pay much more in premiums for less insurance coverage however have the protection of understanding they are secured forever.

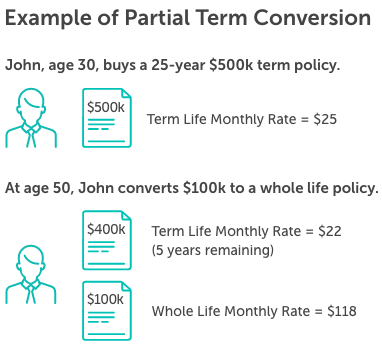

The conversion rider must permit you to transform to any type of permanent policy the insurance provider supplies without constraints - term life insurance with diabetes. The main attributes of the cyclist are maintaining the original health score of the term policy upon conversion (also if you later have health and wellness problems or come to be uninsurable) and deciding when and just how much of the protection to transform

Certainly, total premiums will increase considerably given that entire life insurance is a lot more expensive than term life insurance coverage. The benefit is the guaranteed approval without a medical examination. Medical conditions that develop during the term life period can not cause premiums to be raised. The business may need minimal or full underwriting if you desire to include added cyclists to the new plan, such as a long-term care cyclist.

Entire life insurance coverage comes with considerably higher regular monthly premiums. It is suggested to offer insurance coverage for as long as you live.

Child Rider On Term Life Insurance

Insurance coverage firms set an optimum age limitation for term life insurance policy policies. The costs also increases with age, so a person aged 60 or 70 will certainly pay substantially even more than somebody years younger.

Term life is rather similar to car insurance policy. It's statistically not likely that you'll need it, and the premiums are money away if you don't. If the worst takes place, your household will obtain the advantages.

This plan design is for the client that needs life insurance policy but would love to have the capacity to select just how their cash worth is invested. Variable plans are underwritten by National Life and dispersed by Equity Services, Inc., Registered Broker/Dealer Affiliate of National Life Insurance Business, One National Life Drive, Montpelier, Vermont 05604.

For J.D. Power 2024 award details, visit Long-term life insurance policy creates cash money worth that can be obtained. Policy financings accumulate rate of interest and unsettled plan lendings and interest will reduce the survivor benefit and cash value of the plan. The quantity of money value readily available will normally depend on the sort of permanent plan bought, the amount of protection purchased, the size of time the plan has actually been in force and any outstanding policy fundings.

20 Insurance Life Term Year

A full declaration of protection is discovered only in the plan. Insurance policy policies and/or connected bikers and functions may not be available in all states, and plan terms and conditions might vary by state.

The main distinctions in between the different kinds of term life policies on the market involve the size of the term and the insurance coverage quantity they offer.Level term life insurance policy features both degree costs and a degree survivor benefit, which suggests they stay the very same throughout the duration of the plan.

It can be renewed on an annual basis, but premiums will certainly enhance whenever you renew the policy.Increasing term life insurance policy, additionally called a step-by-step term life insurance policy plan, is a plan that includes a survivor benefit that increases with time. It's generally more complicated and costly than level term.Decreasing term life insurance policy includes a payout that lowers with time. Typical life insurance coverage term lengths Term life insurance coverage is economical.

The major distinctions in between term life and whole life are: The size of your protection: Term life lasts for a collection duration of time and then ends. Average regular monthly whole life insurance price is computed for non-smokers in a Preferred health category, getting an entire life insurance coverage policy paid up at age 100 offered by Policygenius from MassMutual. Aflac provides many lasting life insurance coverage policies, including entire life insurance policy, last expense insurance policy, and term life insurance coverage.

{kind=link}

Latest Posts

What Type Of Insurance Is Final Expense

Selling Final Expense Insurance By Phone

Paying For A Funeral With Life Insurance